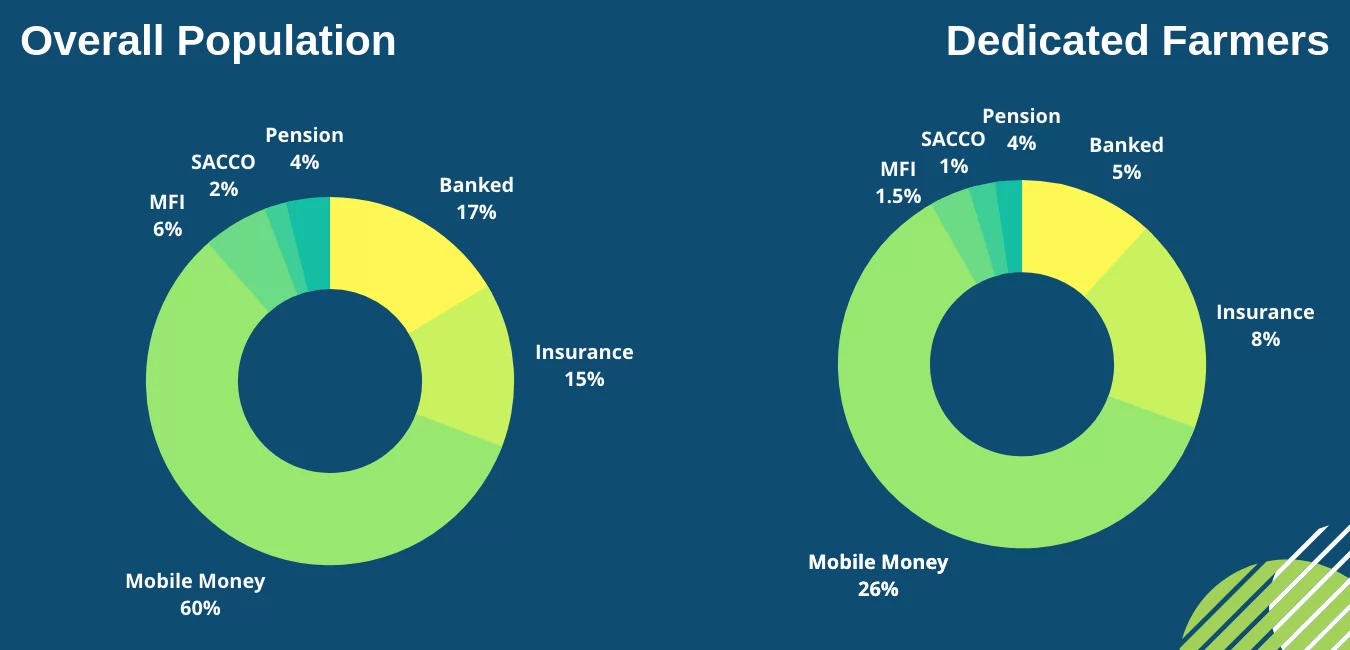

FSDT studies have shown that addressability is not a key issue for the agricultural sector, as the majority of farmers live within 5km of a financial access point and have access to a mobile phone. Although their basic uptake across services has also been increasing, there are opportunities to expand uptake further and to deepen customer usage. Perceptions persist among financial service providers of high risk and low returns for this sector, resulting in few use cases and solutions that meet the needs of agricultural workers.

FSDT studies have shown that addressability is not a key issue for the agricultural sector, as the majority of farmers live within 5km of a financial access point and have access to a mobile phone. Although their basic uptake across services has also been increasing, there are opportunities to expand uptake further and to deepen customer usage. Perceptions persist among financial service providers of high risk and low returns for this sector, resulting in few use cases and solutions that meet the needs of agricultural workers.

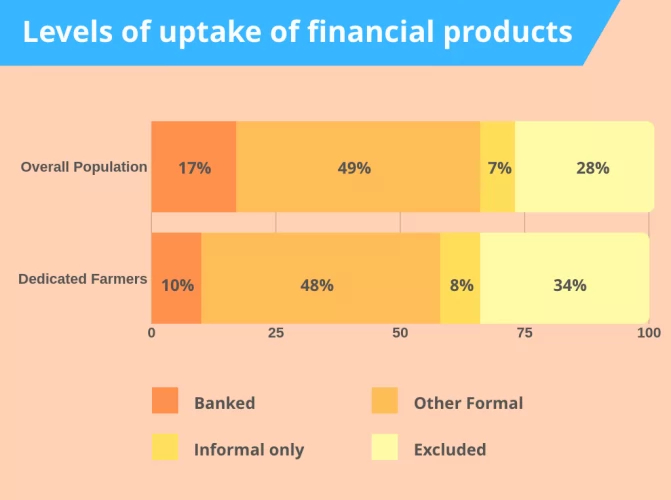

For agricultural workers, the benefits of improved access and usage of financial services are considerable, but many face a range of barriers to inclusion:

- A large majority of farmers live in rural areas, reducing their connectivity to a wide range of formal financial products and services

- Very few have completed secondary education and so have low levels of literacy and numeracy, leading to lack of awareness and knowledge of the benefits of financial products and services

- Average income of dedicated farmers is seasonal and over 10% below national average, presenting challenges to meet registration requirements for formal financial services

- Less than half of farmers own land and, among them, the majority do not have proof of ownership, limiting their ability to meet Know-Your-Customer requirements

FSDT recognises the significant potential offered by inclusion of farmers in the financial sector. In our role as a thought-leader, we are gathering and sharing evidence to encourage financial service providers and policy-makers to develop market-led solutions and for farmers to see how the benefits of formal services could improve the livelihoods of their families and communities. Galvanising new thinking and building capacities on both the supply and demand sides of the agricultural sector is a key priority across all our work.

FSDT recognises the significant potential offered by inclusion of farmers in the financial sector. In our role as a thought-leader, we are gathering and sharing evidence to encourage financial service providers and policy-makers to develop market-led solutions and for farmers to see how the benefits of formal services could improve the livelihoods of their families and communities. Galvanising new thinking and building capacities on both the supply and demand sides of the agricultural sector is a key priority across all our work.